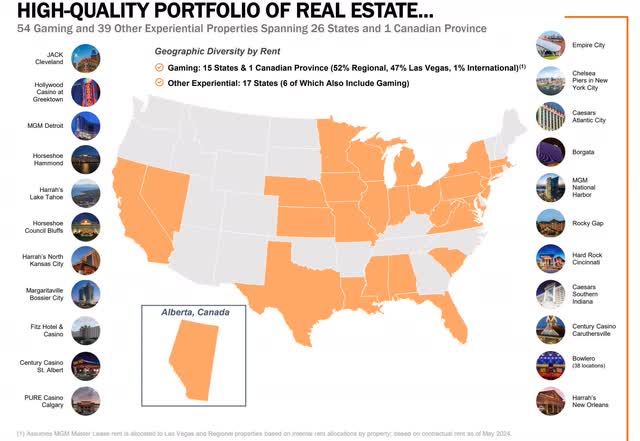

VICI Properties (NYSE:VICI) is a REIT that has focused on prime property ownership in Las Vegas, but it also owns real estate in other areas including Chelsea Piers in New York. Its focus on gaming and hospitality has led it to acquire Harrah’s Las Vegas, Caesars Palace Las Vegas, MGM Grand, The Venetian Resort Las Vegas, as well as many other high profile assets totaling 127 million square feet. With many top hospitality companies leasing these properties from VICI Properties, the rent payments are just about as sure as can be and very long term as well. This makes it an ideal stock for income investors and a recent pullback in the stock makes it even more attractive. Let’s take a closer look:

ViciProperties.com

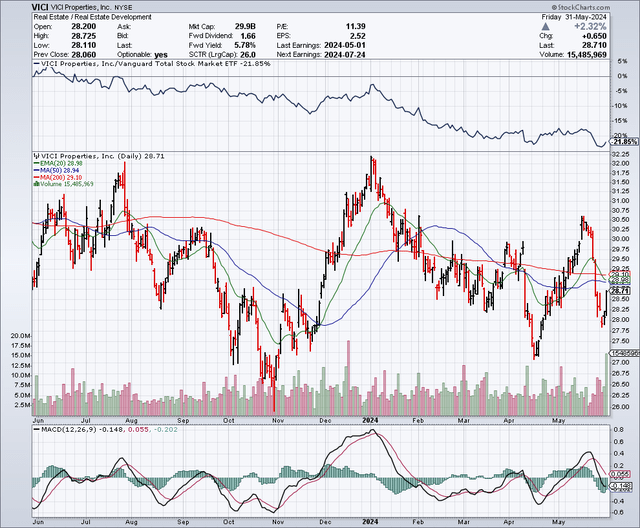

The Chart

As the chart below shows, this stock recently traded up to just over $30 per share, but like many REIT stocks, it has had a pullback as investors weigh “higher for longer” interest rates which impacts this sector in a significant way. The 50-day moving average is $28.94 and the 200-day moving average is at a very similar level at $29.10. I believe the recent pullback is a buying opportunity, especially since this stock is just a bit below these moving averages.

StockCharts.com

Earnings Estimates And The Balance Sheet

Analysts expect this company to earn $2.55 per share in FFO for 2024, on revenues of $3.83 billion. For 2025, FFO is expected to rise to $2.67 per share, with revenues coming in at $3.93 billion. This implies a price to earnings ratio of about 11, which suggests this stock is undervalued when compared to peers. (More on valuation below.)

As for the balance sheet, VICI Properties has about $17.61 billion in debt and around $485.32 million in cash. Moody’s has given this company a “BA1” credit rating with a positive outlook.

Growth Outlook

This company has guided for FFO growth of about 4% for 2024. I expect that future and potentially higher FFO growth will come in 2025 and beyond will come from additional real estate acquisitions. It will also come from inflation-adjusted rent increases, which compound while many expenses for VICI properties remain fixed. However, I don’t see FFO growth as the catalyst for my investment thesis in this stock; my thesis is based on my belief that interest rates will be significantly lower in the next couple of years, and this belief is based in large part on the forecasts from the Federal Reserve.

The Dividend

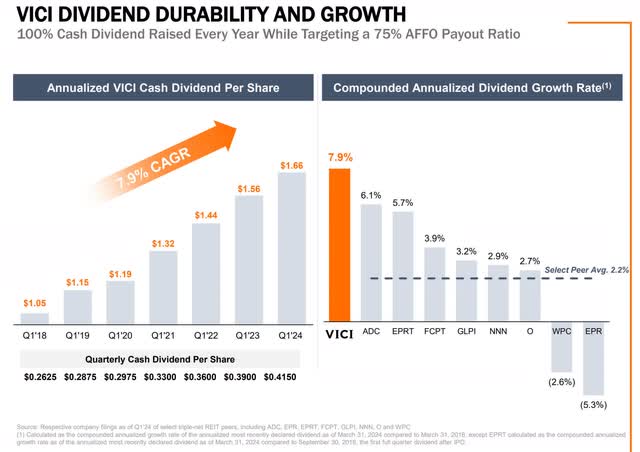

VICI Properties has been an ideal stock for dividend growth. In 2018, VICI Properties paid a quarterly dividend of $0.18 per share. But thanks to consistent increases, the dividend has more than doubled to $.415 per share. On an annual basis, the dividend totals $1.66 per share and provides a yield of nearly 6%. The payout ratio is about 66%, which leaves ample room for fluctuations in profits without causing concerns about the security of the dividend. As shown below, VICI Properties is targeting a 75% AFFO payout ratio for the dividend, so this also suggests more potential increases in the dividend. It also shows that for the past few years, this company has provided a much stronger dividend growth rate when compared to peers.

ViciProperties.com

Valuation

VICI Properties appears undervalued when compared to some of the largest and very popular REIT stocks such as Realty Income (O). For example, Realty Income is expected to deliver FFO of $4.23 per share for 2024. At a current price of about $53 per share, this suggests a PE ratio of about 12.5.

Agree Realty (ADC) is another popular REIT for investors and it is expected to earn $4 per share in FFO. Based on the current share price of nearly $61, this implies a PE ratio of just over 15.

Gaming and Leisure Properties (GLPI) fills a similar niche within the REIT sector since it also focuses on casinos and hotels. Analysts expect this company to earn $3.76 per share in FFO. Based on the current share price of about $45, this puts the PE ratio at 12. While this is similar but slightly higher to the PE ratio for VICI Properties (which is around 11), I believe the property portfolio is not at the same level and therefore does not deserve the same valuation. VICI Properties owns multiple iconic properties in the gaming sector and I believe it deserves a premium for this reason.

Interest Rates Could Be Poised To Plunge Between Now And 2026

In Q1 2024, the Federal Reserve released forecasts which imply a significant drop of 2.25 points in the Fed Funds rate, by the end of 2026. This would imply a reduction in the Fed funds target rate from the current range of 5.25% to 5.5%, to a range of 3% to 3.25%. This would greatly reduce the yield on money market funds, potentially down to around the 3% level as well. Investors who are currently collecting a 5%+ yield in a “risk free” money market fund could be about to realize that there is a big opportunity risk in staying invested with money market funds for too long because the yields could plunge quickly and leave investors looking for other alternatives to maintain the income stream they have become accustomed to.

I believe too many investors are “offsides” right now with heavy allocations to money market funds. When the yields on these funds likely plunge there is going to be a massive amount of cash potentially looking for a new home. According to the latest data from the Federal Reserve, there is about $6 trillion parked in money market funds right now. I believe when rates eventually drop, the REIT sector is poised to be a beneficiary, as income investors scramble to reallocate funds to higher yielding assets. This should lead to a higher share price for VICI Properties and other high quality REIT stocks.

My 2026 Share Price Projections

If money market yields drop by about 40%, to the low 3% range, I believe VICI Properties shares could support a yield around 4% to 4.5%; this means the valuation could be re-rated to a higher level. Based on an annual dividend of $1.66 per share, a yield of 4% implies a share price of about $40. I think this calculation is conservative and it is based on the current premium, whereby VICI Properties now yields less than 1% more than a typical money market yield of just over 5%. In my projections, I am suggesting a future premium of about 1% to 1.5% over money market yields, which is more than the current premium. Therefore, investors that buy this stock now at around $29 per share could be poised to see capital gains of nearly 40% between now and the end of 2026, plus collect the (locked in) yield of nearly 6%, which means total returns could approach 50% in the next couple of years or about 25% on an annualized basis.

Potential Downside Risks

An actual or even perceived slowdown in tourism and gaming revenue in Las Vegas could impact investor sentiment and the share price of this stock. With a focus on hospitality, and on Las Vegas, this REIT might be perceived to be less recession-resistant than other REIT stocks.

The REIT sector is very interest rate sensitive, and that has led to generally poor performance in these stocks over the past couple of years as interest rates have been rising. The Federal Reserve is expected to start reversing these rate hikes later this year; however, inflation is proving to be stickier than expected and some market watchers and analysts believe the Fed will have to keep rates higher for longer or perhaps even raise rates further. In this scenario, where rates stay high or go even higher, REIT stocks could remain challenged and even decline further.

REIT stocks plunged during the Covid market correction in 2020. This indicates that some type of potentially significant economic shock could be another potential downside risk to consider.

In Summary

While the yield of nearly 6% might not be so exciting at a time when money market funds yield just over 5%, things are likely to change in the next year or two with the Federal Reserve forecasting a plunge in rates. In the next couple of years, it is possible for the Fed Funds Rate and money market fund rates to decline into the 3% range, and that could spark significant investor interest in REIT stocks. Based on this scenario, these shares could experience significant upside. I expect strong total returns over the next couple of years due to the combined powers of a nearly 6% dividend yield and share price appreciation, which could provide total returns of 25% on an annualized basis.

No guarantees or representations are made. Hawkinvest is not a registered investment advisor and does not provide specific investment advice. The information is for informational purposes only. You should always consult a financial advisor.

Read the full article here