Intel stock is not loved by Wall Street

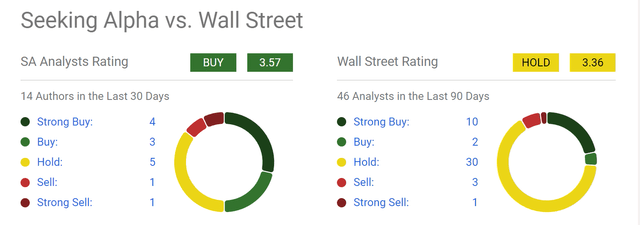

Readers familiar with my writing know that we have been arguing against Wall Street’s opinion on Intel Corporation (NASDAQ:INTC) in the past 1 year or so. As illustrated by the chart below, Wall Street’s sentiment on the stock is at best lukewarm. Overall, Wall Street analysts have a “Hold” rating on the stock, with 30 out of 46 analysts giving it this rating in the last 90 days. Although there is a bit of variance among the analysts. A total of 10 analysts gave it a “Strong Buy” rating and 4 analysts gave it a “Sell” or “Strong Sell” rating.

Seeking Alpha

I, on the other hand, have been bullish on the stock. As argued in my recent article, my view is that:

… the recent price corrections reflect near-term market reaction and present a buying opportunity for investors who have an investing timeframe of 3-5 years. Analysts expect EPS to grow at a CAGR of 20%+ in the next few years and we see such a growth curve as very plausible thanks to a range of catalysts.

My argument in that article was based on a range of catalysts, with the top 3 being “the recent $8.5B cash grant from the Biden administration, secular demand for semiconductors, and margin expansion potential.”

In this article, I want to reiterate our bullish view by focusing the discussion on its foundry business. The goal is to explore this aspect in more depth and to show A) why this INTC’s 3~5 years investment, and B) why the market’s reaction to its quarterly progress (or the lack of it) is overblown and misplaced.

Intel stock: the foundry situation

INTC’s stock prices have been on a roller coaster recently. The stock prices have become so overly sensitive to its foundry news and so detached from business fundamentals to me. For example, the main reason for the large price drop in the past 2~3 months (more on this later) was INTC’s recent disclosure about its foundry business. The disclosure reported a larger-than-expected loss. More specifically,

“the foundry business had an operating loss of $7B on revenues of $18.9B for its Foundry business in 2023, wider than the loss of $5.2B recorded in 2022 on $27.5B of sales.”

I know the foundry business will be a long-term investment for INTC from the beginning, and there will be roadblocks along the way. For such a large endeavor, delays in building new fabs (fabrication plants) and financial losses in their current foundry business are inevitable and don’t bother me too much. The reasons for my bullish view involve a bit of technical background and some engineering details (BTW, I have a pretty good technical background from graduate school and love understanding technical/engineering issues). For those of you who share a similar interest/passion, I’d like to point you to a recent article entitled Understanding Intel’s Foundry Situation. The author did an impressive job on the engineering front and went into technical depth far more than I ever dared to go in my public articles.

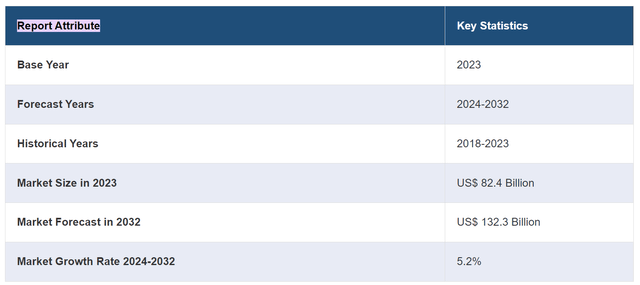

As detailed in my earlier article, I see good odds for Intel Foundry to enjoy margin expansion (say around 40% non-GAAP gross margins and 30% non-GAAP operating margins in the next 3~5 years) and reach a break-even point. Intel projects the foundry business to attract external customers with revenues exceeding $15 billion by ~2030 and become the world’s second-largest foundry by then (after Taiwan Semiconductor (TSM), TSMC). Of course, INTC will be a distant second even if this goal is reached. And furthermore, as many bears have already pointed out, INTC’s fab technology will be very behind TSMC and thus won’t be able to compete for the more lucrative deals. However, my view is that A) the global demand for fab capacity will grow secularly at a robust pace (see the data provided by IMARC below), and B) the demand will grow across various application segments and not only in the most advanced chips demanding the most cutting-edge fab technologies.

As the IMAR report pointed out (the emphasis was added by me):

The global semiconductor foundry market size reached US$ 82.4 Billion in 2023. Looking forward, IMARC Group expects the market to reach US$ 132.3 Billion by 2032, exhibiting a growth rate (CAGR) of 5.2% during 2024-2032. The market is experiencing steady growth driven by the rising demand for advanced electronics across various sectors, including consumer electronics, automotive, and telecommunications, the escalating shift towards electric and autonomous vehicles, and the increasing adoption of AI and machine learning.

The bottom line is that I see a robust demand for INTC fabrication capabilities in the years to come, even if they are not the most advanced. Finally, an addition of $15B in extra revenue is already significant, especially considering INTC’s compressed valuation metrics today. INTC is trading at a 2.6x P/sales ratio as of this writing, vs. TSM’s 11.5x P/sales ratio on a TTM basis.

IMARC report

Other risks and final thoughts

Another bullish consideration in the near term involves the stock’s recent trading pattern, as shown below. And you can also see how severely the stock was oversold in April after it released the update on its foundry business. More specifically, the top panel of the chart shows the price-volume information for INTC stock with its 20-day moving average. The bottom panel shows the Relative Strength Index (“RSI”). I see several textbook signs for INTC stock prices to move up in the near term.

First, the price just crossed above the 20-day moving average. The current price of $33.99 is positioned decidedly above the 20-day moving average of $31. Second, the strong price rallies in the past few days were also accompanied by expanding trading volume, a textbook combination that indicates an upward trend. Finally, its RSI has moved out of the oversold territory. The RSI is currently at 72.56. An RSI reading of 70 or above is generally considered to be in the “bullish territory.” Also note that the RSI itself has been trending upward since July, suggesting that the selling pressure has eased and the buying pressure is picking up.

StockCharts

In terms of downside risks, besides the execution challenges in their foundry business, INTC also faces a few other risks. The ongoing global trade tension (especially between the U.S. and China) and the potential for an economic slowdown are some key macroeconomic risks facing both INTC and its chip peers. On the emerging artificial intelligence (AI) front, the competition will only become more intensified not with heavyweights such as Nvidia (NVDA) and Advanced Micro Devices (AMD) but also with new entrants. Many non-chip tech firms (such as Apple, Google, etc.) have started investing in their own AI chips recently. Finally, INTC derives a large portion of its revenues from the PC segment. The segment’s growth could be limited as PCs reach saturation and other alternative computing devices (mobile, cloud, etc.) become more and more mainstream.

All told, with all these uncertainties, I think it is proper to say that Intel Corporation is currently in a state of flux. It is certainly a high-risk investment that I won’t recommend to more conservative investors. However, my view is that it has the financial wherewithal and technical expertise to turn things around. In particular, its foundry business is a long-term investment, and the market’s overreaction to near-term setbacks only creates excellent buying opportunities for long-term investors.

Read the full article here